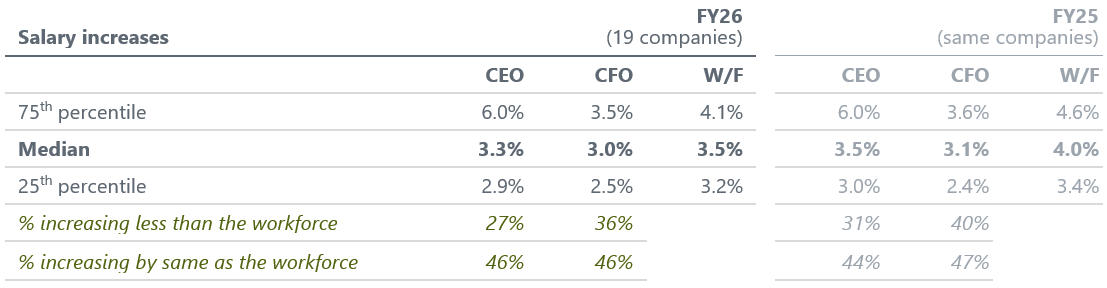

2025/26 Pay Decisions (September year ends)

As we head into the 2026 AGM season, Ellason has reviewed the FY25 and FY26 pay decisions for those FTSE companies with September year ends (a sample of 19 companies based on those which had reported as at the end of January) to identify any early trends.

Median ED salary increases are broadly aligned to the average workforce rate

Almost all companies in the sample awarded salary increases to Executive Directors for FY26, with the median increase remaining closely aligned with that budgeted for the wider workforce and prevailing rates of price inflation. The interquartile range of reported salary increases also remains comparable year-on-year.

Almost half the companies in the sample (46%) increased Executive Director pay in line with the workforce rate for FY26. Companies that increased Executive Director salaries by more than the workforce rate often did so as part of phased arrangements following recruitment or a broader strategy to reposition pay levels relative to competitive market norms.

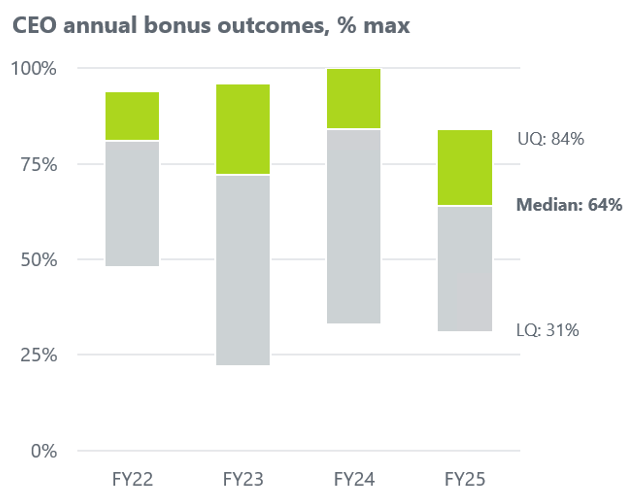

Bonus payouts are mixed

The median CEO bonus payout decreased from 84% to 64% of maximum, following a year of significant and persistent macroeconomic uncertainty. Only 12% of the companies in the sample paid maximum bonuses for FY25, compared to 29% for FY24.

However, lower quartile levels of payout have been more stable (c.30% of maximum). This trend likely results from the structural benefit of a balanced scorecard approach to bonus design that is typical practice in the UK market; the use of multiple measures, both financial and non-financial, helps to maximise the probability of at least some payout.

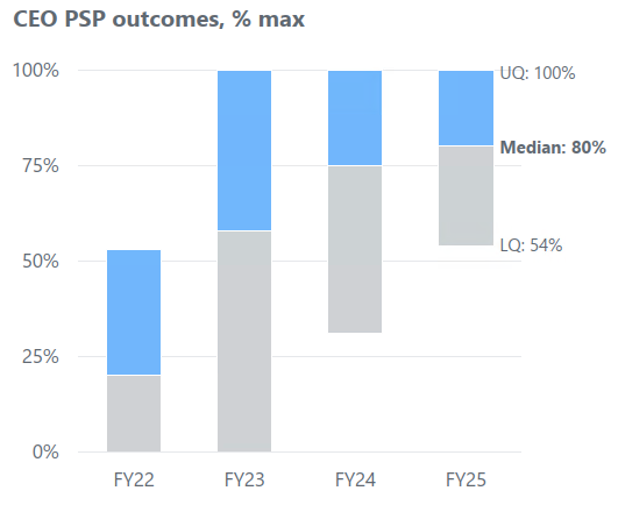

LTIP vesting outcomes are levelling off

Of the companies reporting on LTIP cycles with a performance period ending September 2025, the median vesting outcome has increased slightly, from 75% to 80% of maximum. This is the first LTIP cycle since awards granted in early 2017 that does not include a Covid-impacted year in the performance period. The observed peak in payout levels likely reflects the fact that targets for these awards were set during a period of ongoing uncertainty around Covid and the timing of a broader market recovery. Over time, we anticipate the trend in LTIP vesting to revert to longer-term historical norms.

Some significant changes have been proposed to Remuneration Policies

Seven of the 19 companies (37%) in the sample are renewing their Remuneration Policy for FY26; all are doing so in line with the triennial review cycle. The most common policy change being proposed is to increase the LTIP opportunity (three companies). Two of these companies increased the CEO’s shareholding guideline at the same time (by 50% of salary in each case).

Two companies continued the trend of proposing to soften bonus deferral requirements once the shareholding guidelines have been met by an Executive Director; one company reduced the requirement by 50%, while the other removed the requirement entirely. Across the entire sample, 47% of companies now have flexibility to soften bonus deferral, with an even split between those which lower, and those which drop entirely, the deferral requirement once the shareholding guideline is met.

Future plc introduced a hybrid plan for Executive Directors, i.e. using performance shares alongside restricted shares. Part of the existing PSP opportunity was converted into restricted shares on a 2:1 exchange ratio, with restricted shares subject to a discretionary underpin and ‘3+2’ vesting period. This Policy was supported by 94% of shareholders at the recent AGM.

Ellason commentary

Early indications are that the salary inflation and package design trends observed during 2025 will continue into 2026, while lower bonus outcomes and a levelling off in LTIP vesting levels reflect ongoing macroeconomic uncertainty and volatility in market conditions.

The alignment of pay outcomes to performance outturns remains a key input to voting decisions and proxy advisor recommendations. Investors and proxy advisors continue to advocate for clarity of reporting around decision-making and basing pay proposals on comprehensive, company-specific rationale rather than market comparisons in isolation. Early indications in the 2026 AGM season are that strong shareholder support can be secured for material changes to policy (in terms of structure and/or quantum) if framed by compelling commercial context.

We will be actively monitoring developments in the coming months and will provide further updates.